direct vs indirect cash flow gaap

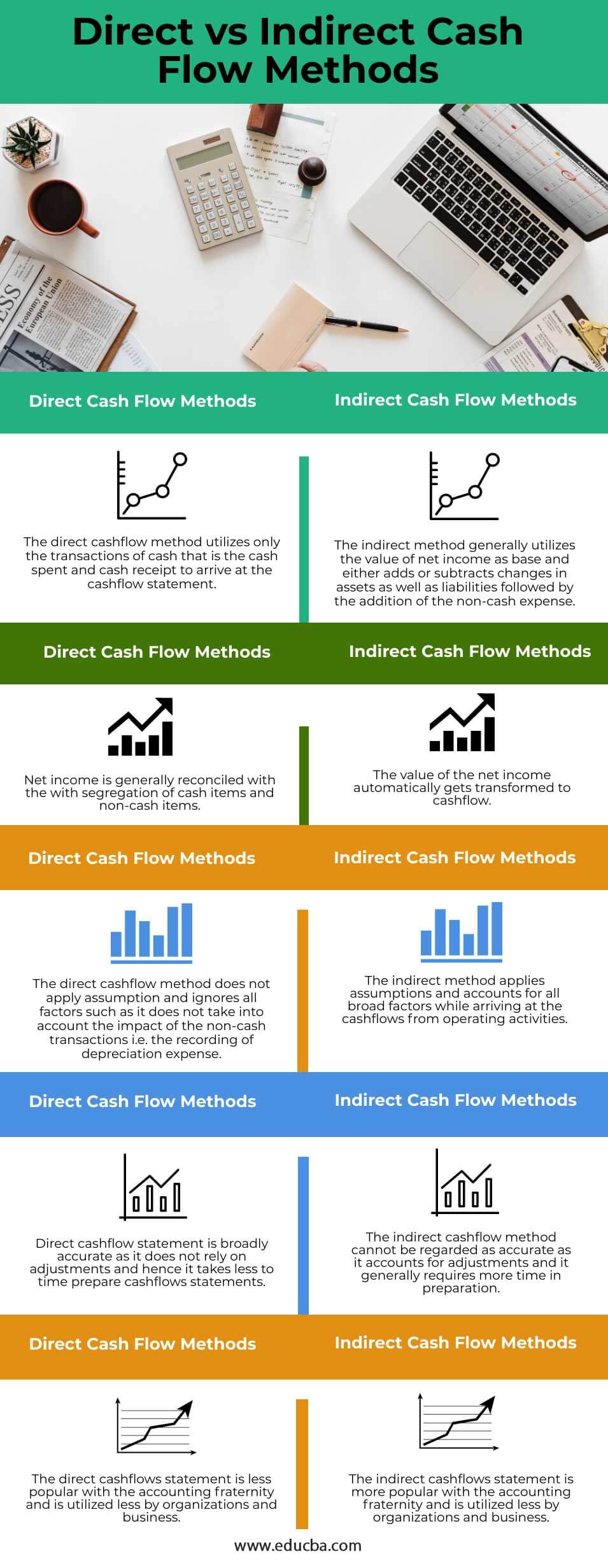

The key difference between direct and indirect cash flow method is that direct cash flow method lists all the major operating cash receipts and payments for the accounting year by source whereas indirect cash flow method adjusts net income for the changes in balance sheet accounts to calculate the cash flow from operating activities. However of the two the direct method is generally encouraged.

The Direct And The Indirect Method For The Statement Of Cash Flows Online Accounting

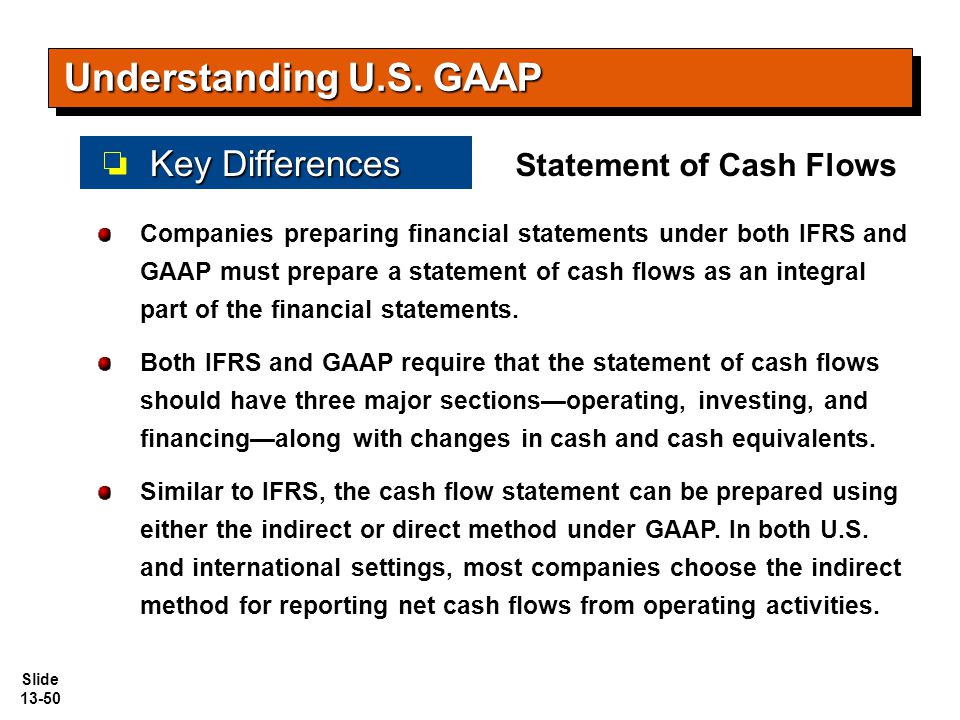

Most companies elect to prepare the Statement of Cash Flows using the indirect method.

. Up to 5 cash back IAS 7 and Section 230-10-45 FASB Statement No. GAAP also calls the indirect method the reconciliation method. Non-cash expenses like depreciation and amortization are ignored in the direct method while they are taken into consideration in the indirect method.

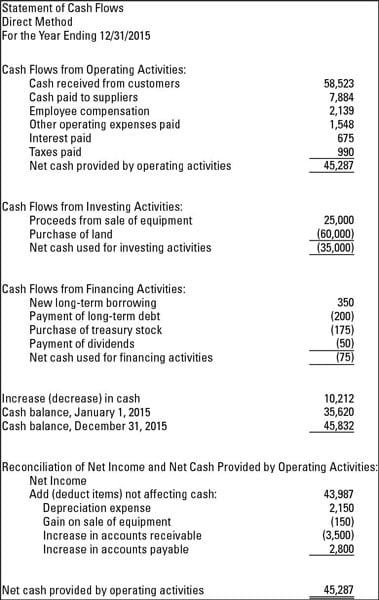

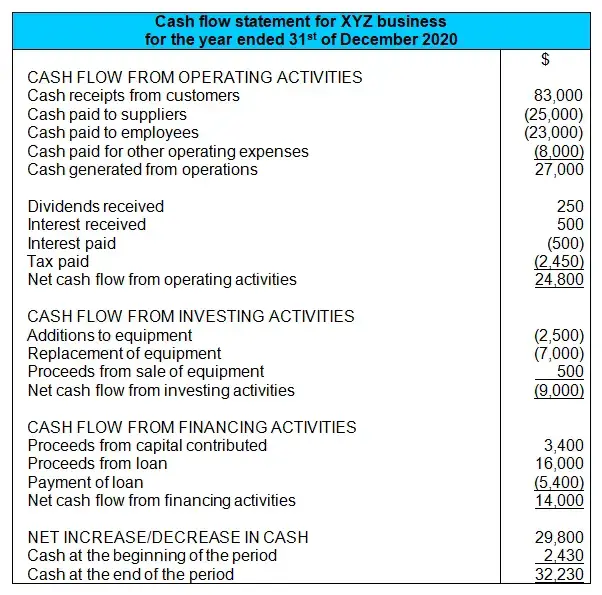

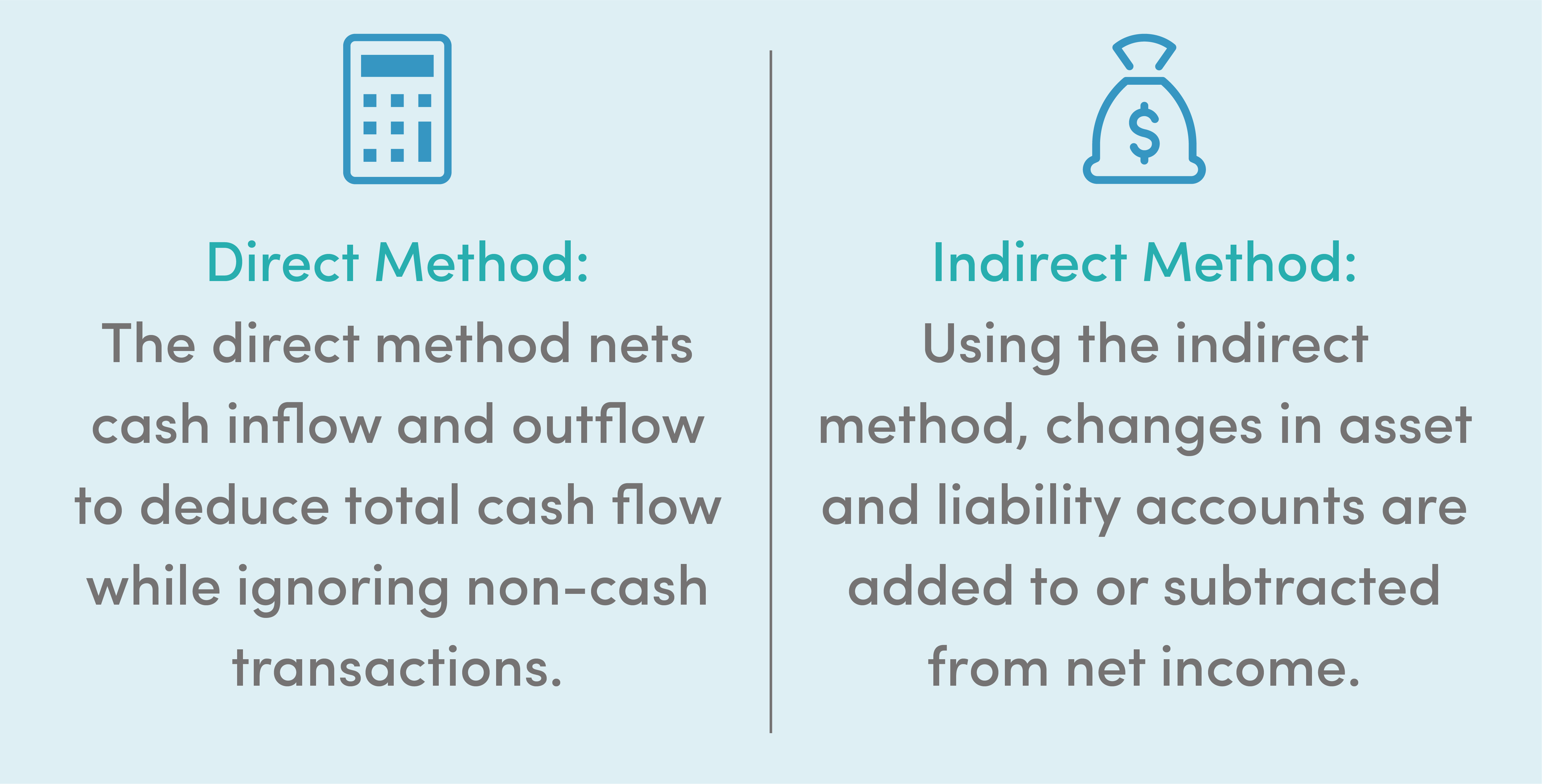

A cash flow statement is an accounting of how money flows through a company. Under the direct method you present the cash flow from operating activities as actual cash outflows and inflows on a cash basis without beginning from net income on an accrued basis. The direct method details where cash comes from and where it goes.

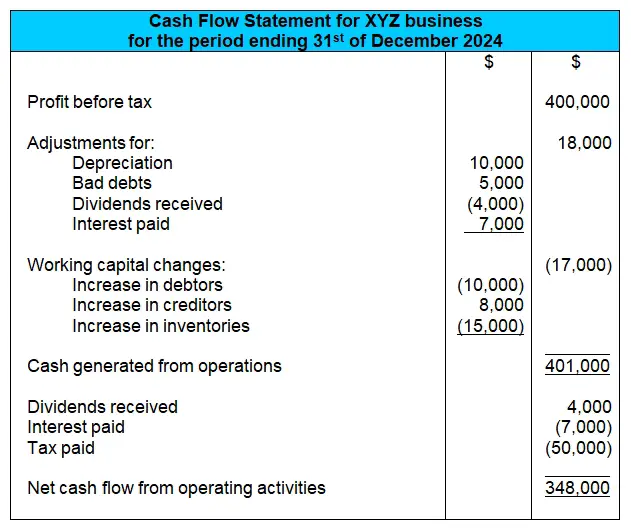

Adjusting net income to operating cash flows is easier and less costly than reporting gross operating cash receipts and payments which is the case in the direct method. While both are ways of calculating your net cash flow from operating activities the main distinction is the starting point and types of calculations each uses. Classified Balance Sheet Income Statement with Gross Profit and Operating Income Loss Indirect Cash Flow Statement US GAAP Cash Flows Statement Indirect Method Tree View of same information Examples of Cash Flow Statement.

Though it may be easy to confuse the two the statement of cash flow is distinct from the income statement. There are no differences in the cash flows from investing activities andor the cash flows from financing activities Under the US. This is because if a company elects to present the Statement of Cash Flows under the direct method the company must then present a reconciliation of net income to cash flows from operating activities in the footnotes to the financial statements.

The indirect method on the other hand focuses on net income and may include cash that is not yet in the business. The second column provides the general structure of the UCA cash flow statement. The UCA cash flow model has become a standard for the lending industry.

Alternatively the direct method begins with the cash amounts received and paid out by your business. The direct method of cash-flow calculation is more straightforward and it shows all your major gross cash receipts and gross cash payments. In contrast the indirect method starts with net income for-profit entities or the change in net assets NFP entities adds back non-cash expenses removes gains and losses and adjusts for the changes in current asset and current liability accounts.

106 Both encourage the use of the direct method. The direct method the income statement is reformulated on a cash basis rather than an accrual basis from the top of the statement the income part to the bottom the expense part. The indirect method backs into cash flow by adjusting net profit or net income with changes applied from your non-cash transactions.

In the direct method reconciliation is used to separate various cash flows from others while in the indirect method the conversion of net income is done in cash flow. Statement of cash flows. 95 permit the direct and the indirect method of reporting cash flows from operating activities.

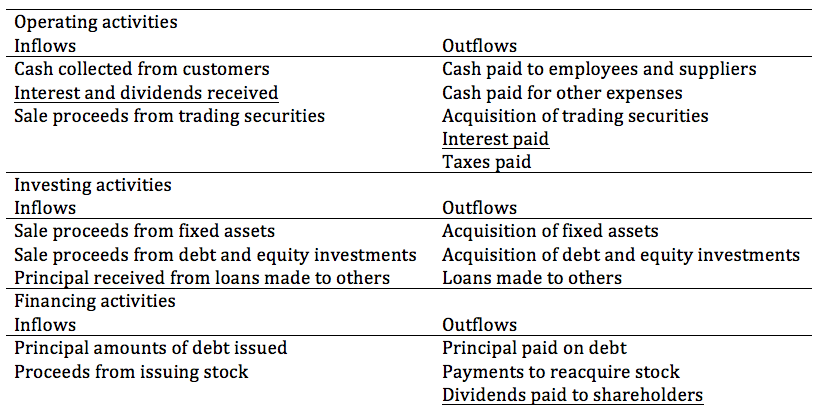

Also if a company. The main difference between the direct method and the indirect method of preparing cash flow statements involves the cash flows from operating expenses. Under the direct method the statement of cash flows reports net cash flow from operating activities as major classes of operating cash receipts eg cash collected from customers and cash received from interest and dividends and cash disbursements eg cash paid to suppliers for goods to employees for services to creditors.

For example if a retailer sells an item on credit the indirect method will consider this as income and reflect this in the figures whereas the direct method wont include it until the bill has been paid. It provides a slightly different view than the FASB 95 indirect and direct models. The indirect method works from net income so the bottom of the income statement and adjusts it to the cash basis.

The direct method is one of two accounting treatments used to generate a cash flow statement. Cash flows from investing activities and cash flows from financing activities are the same for a company regardless of whether the direct method or indirect method is used. Interest received must be classified as an operating activity.

Direct Financing Lease Selling Loss. UCA Cash Flow or Uniform Credit Analysis cash flow is a variation of the FASB95 direct cash flow format. Concept Monetary For Period.

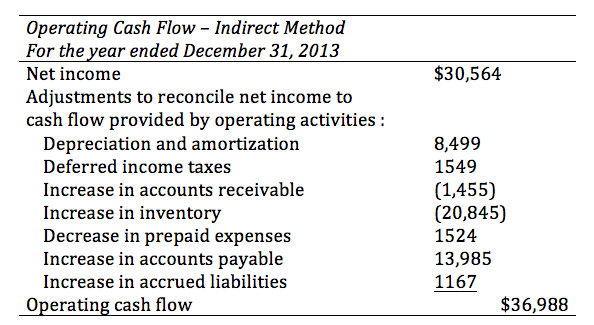

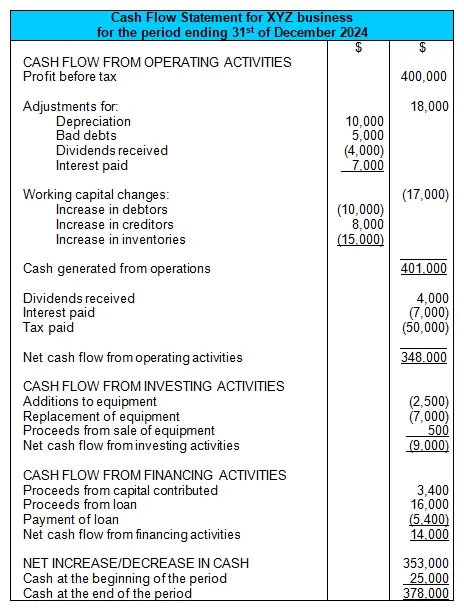

Below is an example of the cash flow from operations segment of a cash flow statement prepared under IFRS using the indirect method. Direct Method or Income Statement Method. However if a company used the direct method it is also required to show reconciliation between net income and cash flow from operations.

GAAP requires a reconciliation of net cash flow from. These financial statements are required parts of a public companys quarterly and annual statements. 108 In addition unlike IFRSs US.

Bank overdrafts are classified as part of cash and cash equivalents Either the direct or indirect method may be used for reporting cash flow from operating activities. The direct cash flow statement method uses actual cash inflows and outflows from business operations instead of changing the operating section from accrual to cash accounting. Main Difference between Direct and Indirect Method of SCF.

The main difference between the direct method and the indirect method of presenting the statement of cash flows SCF involves the cash flows from operating activities. US GAAP also requires similar adjustments. When combined analysts take the cash flow statement the.

The indirect method begins with your net income. Allowing companies to elect to present cash flows from operating activities using either the direct method showing receipts from customers payments to suppliers etc or indirect method profit or loss for the period reconciled to the total net cash flows from operating activities. We will look at both methods with the same data so you can see the.

Preparing The Statement Of Cash Flows Using The Direct Method The Cpa Journal

/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is And Examples

Direct Vs Indirect The Best Cash Flow Method Vena

:max_bytes(150000):strip_icc()/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is And Examples

Direct Vs Indirect Cash Flow Methods Top Key Differences To Learn

Preparing The Statement Of Cash Flows Using The Direct Method The Cpa Journal

27 Understanding Cash Flow Statements

Methods For Preparing The Statement Of Cash Flows Dummies

Preparing The Statement Of Cash Flows Using The Direct Method The Cpa Journal

The Indirect Cash Flow Statement Method

Produce Gaap Compliant Statement Of Cash Flows Reports In Xero Hq Xero Blog

Direct Vs Indirect Cash Flow Methods Top Key Differences To Learn

What Is The Difference Between The Direct And Indirect Cash Flow Statement Methods Universal Cpa Review

The Indirect Cash Flow Statement Method

Statement Of Cash Flows Ppt Video Online Download

27 Understanding Cash Flow Statements

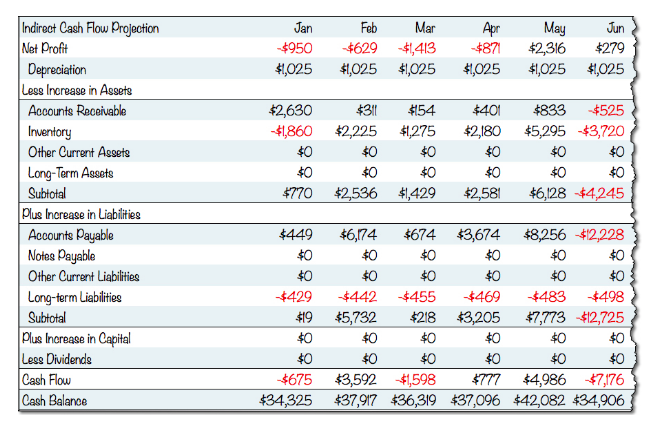

Direct Vs Indirect Cash Flow

/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is And Examples

The Indirect Cash Flow Statement Method